Experience to help users regain control of revolving credit balances before and after delinquency. The solution combined a reactive restructuring flow for users already in financial difficulty, and a preventive relief plan for users showing early risk signals.

Key Takeaways

Debt support is most effective when offered before users fully default.

Financial clarity and transparency are essential in high-stress decision moments.

Preventive intervention can outperform reactive recovery in both user trust and portfolio outcomes.

Designing for financial hardship requires balancing empathy with strong risk controls.

Self-service restructuring reduces operational costs while improving scalability.

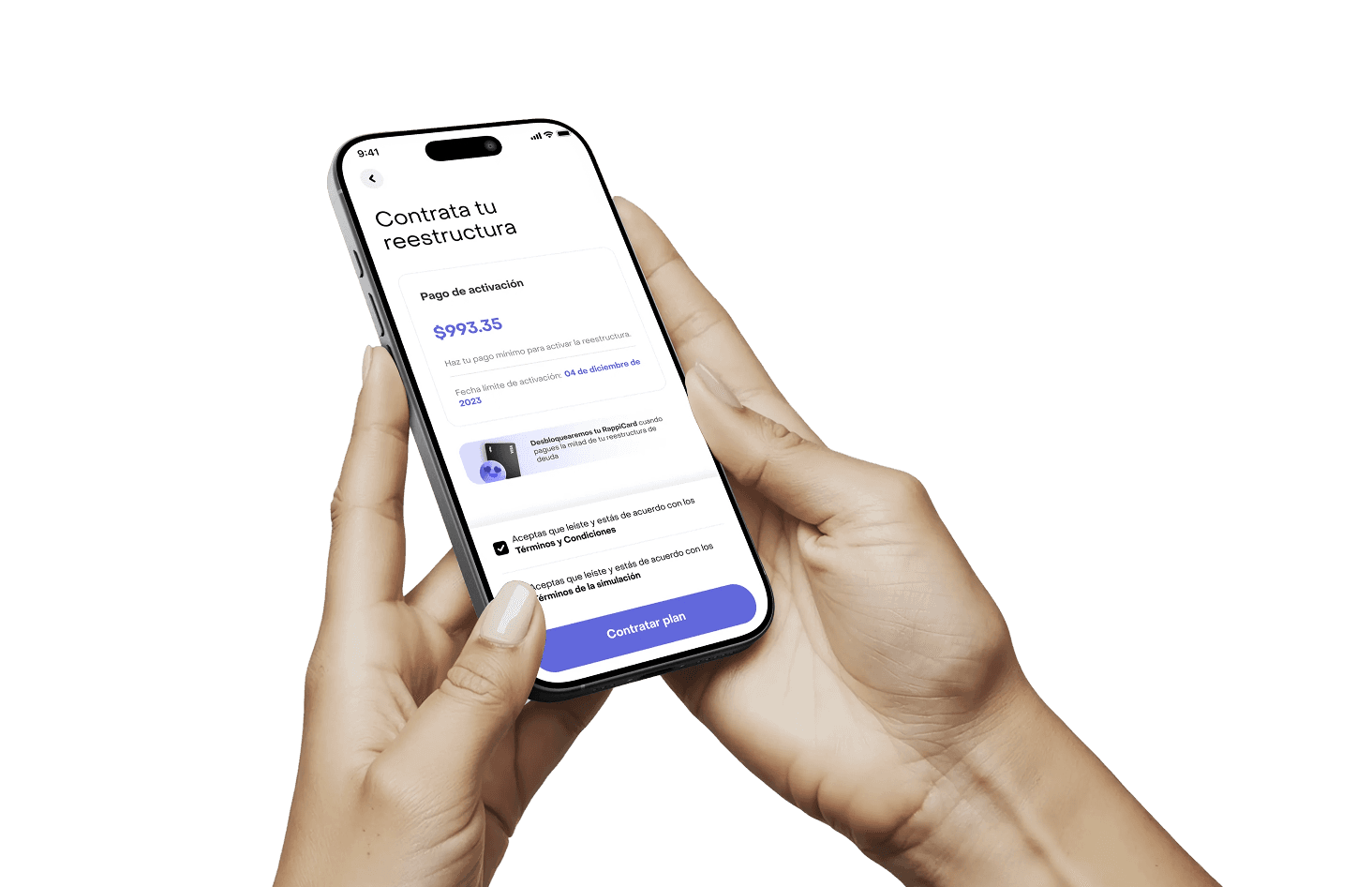

Final solution

Activation payments

work as both trust and risk control

Users commit faster

when repayment options

are transparent

Preventive intervention

reduces delinquency

escalation

Progressive guidance

lowers decision fatigue

Relief is framed as

support, not punishment

Impacted metrics

Cost to serve

Reduced

vs Manual call-center contact restructuring

Risk control

Improved

Higher early and late control recovery of users

Finantial trust

Increased

Improved perceived financial control and trust by self serve

Learning &

growth

I learned that debt relief products are not just transactional flows — they are trust systems.

By evolving restructuring from reactive recovery into preventive support, we demonstrated how fintech can build experiences that protect both:

The user’s financial wellbeing

The business portfolio health